AI in Wealth Management Can algorithms actually outperform human financial advisors

However, 74% of clients still feel that they need a trustworthy human during stressful markets. While the question of AI versus human advice may remain a theoretical conversation, it is a material make-or-buy decision impacting the financial advisory business model for both digital-only firms and high net worth individuals.

Where AI Dominates: Speed, Scale, Precision

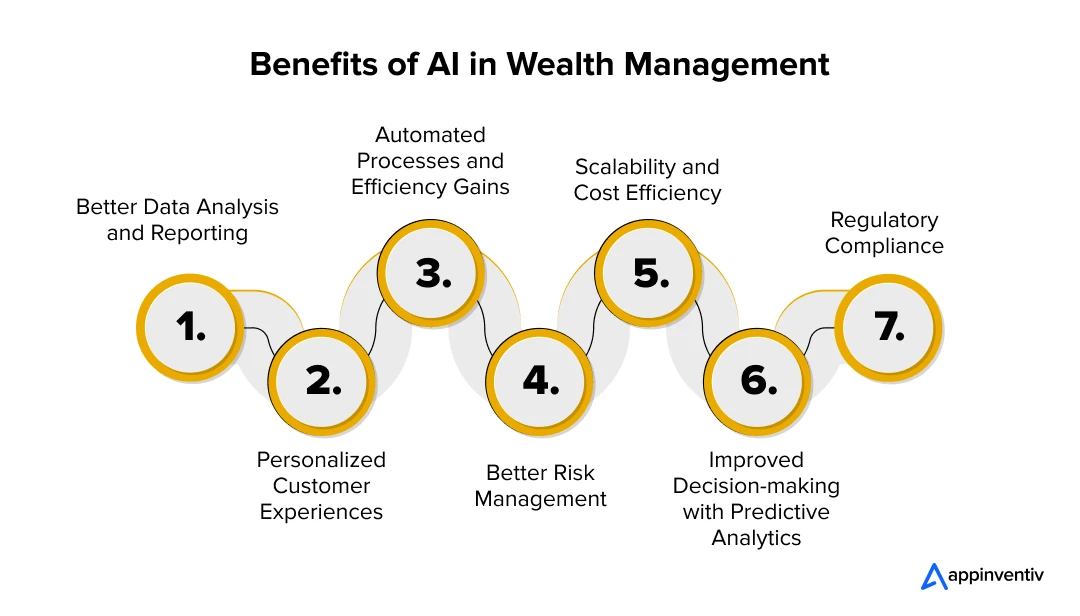

AI platforms for managing wealth are particularly good with quantifiable benchmarks. Systems such as Origin perform exceptionally well, scoring 98.3% against the current Financial Planning Benchmark compared to normal large language models (LLMs), which average 91% to 94% and advisory certified financial planners (CFPs), which have 79.5%, use deterministic engines to produce high-level accuracy with no ‘hallucination’ risks on compounded growth and tax calculations.

Cost structures also favour algorithms. In contrast to hiring a human (1-2%) or a robo-advisor (0.25-0.50%), the average assets under management (AUM) required of each client is $500,000+. Automated tax-loss harvesting occurs daily as a result of continuous monitoring, rebalancing occurs every time a drift is detected and both tax and arbitrage opportunities have been scanned 24/7 long before a human advisor ever reviews them.

The scalability of AI is another primary differentiator. While a single advisor can serve anywhere from 100-150 clients, a single instance of an AI can meet the needs of thousands of clients all at once. Companies like Morgan Stanley have experienced 98% implementation rates from advisors using GPT-4 tools, resulting in a 20% year-over-year increase in revenue as a result of improved workflow automation.

Human Strengths: Context, Trust, Behavioural Guardrails

Humans excel at nuanced judgement and emotional connection, while algorithms fall behind. Generic AI has no verified access to financial information leading to less than average levels of personalisation. Humans are able to form an in-depth understanding of context through years of conversation as well as changes in circumstances like death or divorce or inheritance.

Evidence supports this conclusion. Surveys indicated that between 56 and 74 per cent of respondents preferred speaking to humans regarding retirement planning, whereas just over 13 per cent of respondents expressed willingness to use AI alone. During the bear market in 2022 (when the stock market was down over 40 per cent), robo-advisor outflows were in excess of 25 per cent while human assets under management increased by 8% over the same time period. The provision of behavioral coaching (to stop you from panicking and selling) is an irreplaceable part of the advisory process.

The current regulatory landscape provides more support for humans. There are SEC-registered AI-based advisors that exist, but they are subject to compliance frameworks that require someone - this is a human - to be held accountable for their advice. Goldman Sachs and UBS both exited from their pure-play robo-advisor retail models after their attempts to scale these businesses were unsuccessful.

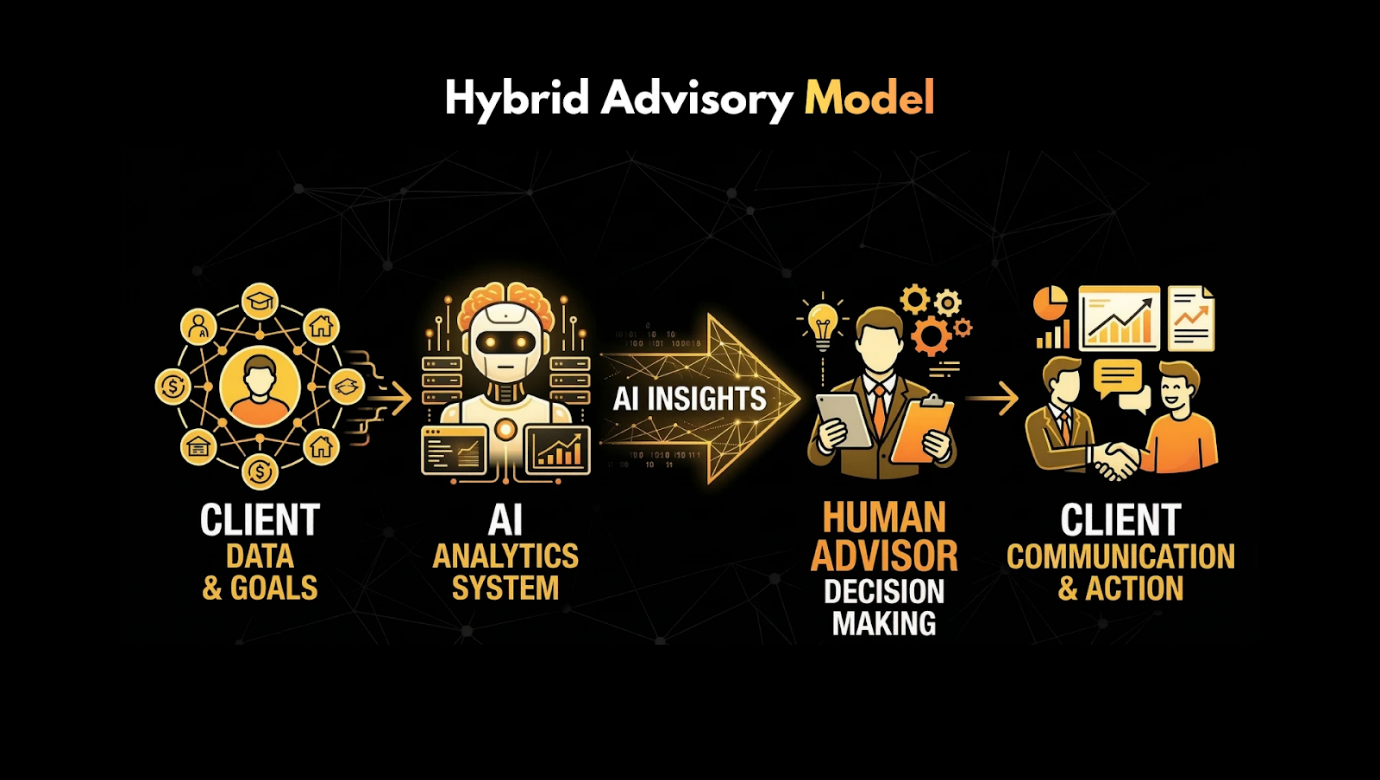

The Hybrid Reality: Augmentation Trumps Replacement

According to a consensus in the financial services industry, hybrid wealth management is likely to be the final outcome. Coach AI from JPMorgan has increased the capacity of its advisors by 50%. Northwestern Mutual refers to AI as a "supercharger" for workflow. Advisors believe that they are able to serve more clients without negatively affecting service quality, resulting in an increase of efficiency between 10% and 20%.

For wealth managers in India, hybrid wealth management is a way of taking advantage of the scale that $1.2 trillion in household savings that have been converted from informal to formal channels will create as a result of the use of AI to handle compliance-heavy KYC/AML requirements, whilst allowing humans to focus on relationship alpha. Platforms that combine the best features of Groww-style automated platforms with the best features of 1MG-style trust will be able to attract the next 500 million retail investors.

Business Decision Framework: HNI vs. Mass Affluent

Wealth managers will need to segment clients in a very strategic way moving forward—artificial intelligence will outperform humans on simple and repeatable (scalable) mandates, while humans outperform AI on complex, trust-dependent relationships. For simple portfolios under $1 million in assets, algorithms provide better execution than humans through non-discretionary (rules-based) strategies such as target-date funds, tax-loss harvesting, and constant online monitoring and rebalancing at extremely low prices (24/7). Mass affluent clients (the majority of these clients), who are very cost-conscious, focus more on efficiency than on getting "hand-holding" type services, will pay 0.25 - 0.50% of AUM fees—with no minimum AUM—while freeing up additional capital to invest for compounding.

In contrast, where there is nuance, humans can create alpha. This is especially true for complex situations with multiple variables (cross-border taxes, generational wealth transfers, and/or philanthropy) that require context-dependent judgment that is not currently available from any algorithm. Clients with more than $5 million in assets will need customized solutions (liquidity management/wealth transfer/alternative asset allocation) that utilize the relationship that exists between the client's advisor and their family. Further, during periods of market volatility, advisors mitigate the effects of panic selling through behavioural coaching—consistently achieving a 92% advisor-retained AUM through 2022 drawdown, while robo-advisor outflows are only at 25%. For family offices, which require decades of trust-based relationships to navigate through regulatory changes and family dynamics, the assignment of family office mandates is predicated on trust—the advisor and the family have known each other for decades.

Progressive organizations have a hybrid stack model with AI as default for 80% of mass affluent clients, with seamless human escalation for edge cases. They have a tiered pricing where robo-core execution is based on 0.3% AUM, hybrid augmentation is based on 0.8% AUM, and white-glove service providing to HNI clients is 1.2% AUM. This structure reflects delivery economics by allowing for both scale and premium, therefore augments can create a competitive advantage.

Indian Opportunity: Scale Meets Trust

The competition to be the number one Wealth Tech platform in India is heating up quickly. Zerodha Coin, Upstox Pro, and Fisdom are piloting AI Portfolio Builders but will ultimately rely on distribution through the networks of their respective human RM's to acquire clients. With over 2,500 RIAs now registered with SEBI, this event has created hybrid distribution on a large scale.

THE PLAY is an AI-first platform that will use human "Conductors" to distribute premium tier solutions. Family Offices with $50-500 Cr AUM will want both; algorithmic efficiency combined with inter-generational stewardship.

The Verdict: Teamwork Beats Tournament

Wealth management will not be replaced by artificial intelligence but will instead be transformed. Algorithms manage problems while the people provide solutions. Clients benefit through the combination of human empathy and the accuracy of hybrid execution. Firms that do not consider this relationship will have their margins reduced from below or be disrupted from above.

The most sophisticated allocators are asking for adviser augmentation and adopting an augment or replace approach for their advisers will restrict themselves to managing the wealth of the past.

Latest Posts