Beyond the Bank How P2P Lending Platforms Are Offering Better Returns Than Traditional Savings

Why Money Is Walking Out of Savings Accounts

Globally, the way of saving is changing, as we have started to become more inclined towards higher-yielding investment products. For instance, in India, more and more people have been moving their savings out of traditional bank deposits, which yield low returns of around 3% to 4%, to other investment products such as debt funds, hybrid funds, and now regulated peer-to-peer lending platforms. This trend is expected to continue, particularly as borrowers of money earn double-digit interest rates on their loans while the spread between the interest rates on loans and what banks are paying on deposits is very wide.

Based on past performance data, platforms like LendingClub have produced P2P portfolios that have outperformed traditional fixed income investments with average annual returns between 8.8% and 13%, respectively. P2P lending case studies in India after the introduction of regulation indicate net returns as high as 10% to 15% after adjusting for defaults and any associated fees. Even if these returns are generally lower than some types of fixed deposits, they are still significantly higher than the average bank deposit.

How P2P Lending Actually Works

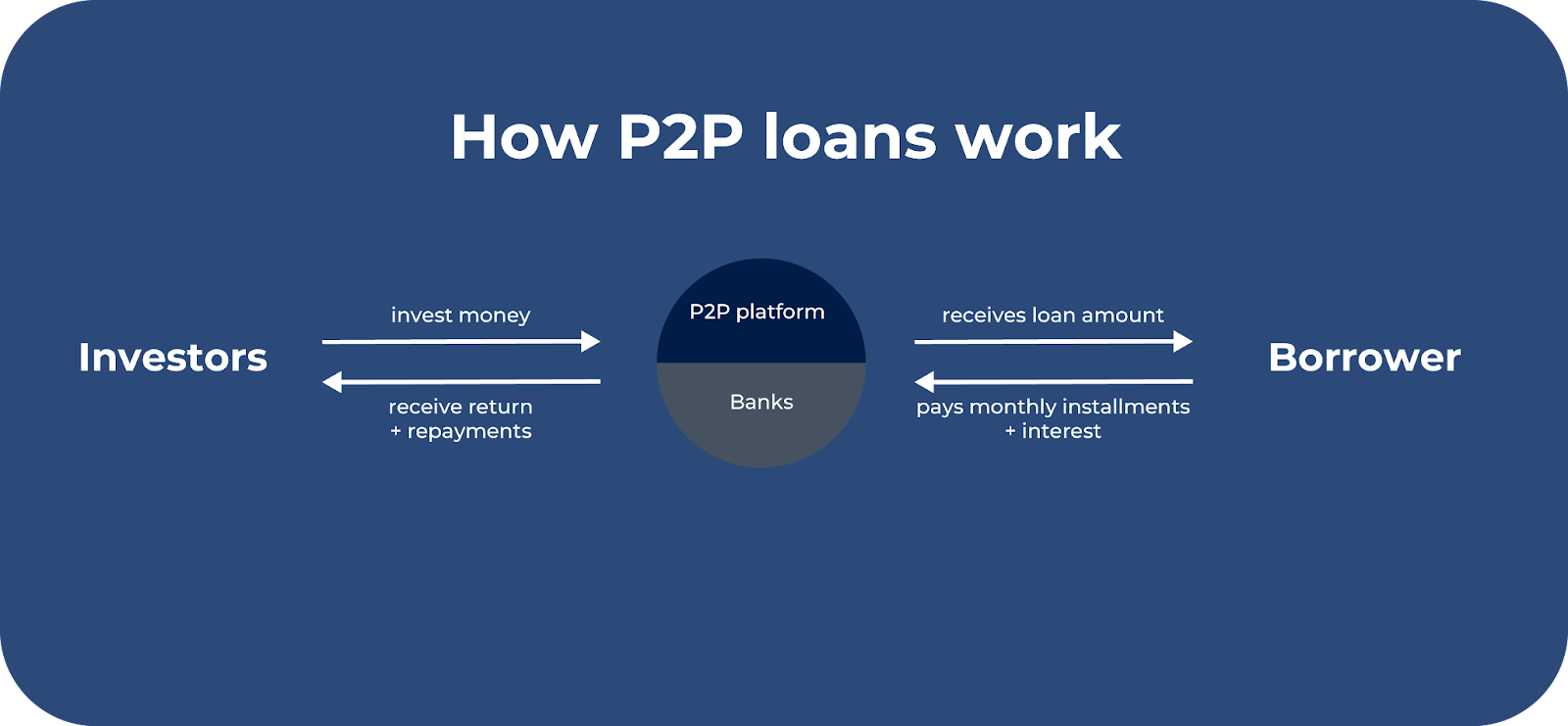

The primary concept behind peer-to-peer lending is that the bank will not be the principal in any transaction conducted using a peer-to-peer platform. The RBI-registered Non-Banking Financial Company- Peer to Peer (NBFC-P2P) platforms simply connect individual lenders and borrowers; therefore, neither the loans nor the platform will be included on the bank's or the NBFC-P2P's balance sheet. When assessing a borrower's creditworthiness, the NBFC-P2P platforms use traditional credit bureau reports, as well as newly developed artificial intelligence-based scoring models, that very significantly help assess risk. Once a borrower has been approved for a loan, the lender will distribute his or her capital over many loans (on average 50-100 small dollar amount loans).

Most P2P platforms in India will charge an average of 18-24% for borrowers while charging an average of 2-3% per year for their services. One example from one leading P2P platform illustrates that a portfolio of 10 lakh rupees over 500+ loans, at a borrower rate of 24% (with a 3% non-performing asset assumption), can produce an internal rate of return of between 12% and 15%. This type of financial product is especially attractive to high-net-worth individuals (HNIs) and technologically savvy retail investors.

The Regulatory Reality Check in India

As of November 2024, RBI has created stringent P2P Guidelines, which you will find to be beneficial when you read through the detailed policies.

Some of the features of these new Guidelines will be as follows:

- Platforms are prohibited from guaranteeing or providing so-called “assured” investment products or the same.

- All lenders are to take the full risk of default, and they cannot provide any credit improvement for the lender.

- There is now a combined exposure limit of ₹50 lakh for each lender across all peer-to-peer platforms and in order to issue loans above ₹10 lakh, the lender must be able to establish that they possess a net worth of at least ₹50 lakh.

- Cross-selling of products is to be heavily limited. In that only loan-specific insurance can be sold on each platform, and that each platform must be very clear to the lenders as to what the lending guidelines will be.

Are Returns Really “Better” Than the Bank?

Theoretical returns as shown on paper and actual returns received depend significantly upon how you've structured and managed your portfolio of investments through P2P lending. Historical returns from diversified and diversified P2P lending portfolios in developed markets have typically provided 6%-8% returns while investors who are more accepting of higher credit risk have earned even higher rates of return.

Compared to the returns offered by deposit accounts for either fixed deposits or savings accounts, the range of actualised returns for a reasonable amount of time following performance defaults while using P2P lending to invest in Indian businesses can be very good; as post-defaults are producing annualised returns of 10%-15% depending on whether or not NPAs remain under control and whether repayments are reinvested.

When you look at the kind of rates available for a fixed deposit account (6%-7%) and a savings account (3%-4%), the significant deferential between those returns is evident as those rates of return are generally less than inflation. You can clearly see that as your rate of return potential increases, your exposure to higher levels of risk versus earning lower levels of returns increases. As a risk aware investor, the important question is not, "Is P2P better at offering returns than a fixed deposit?" but rather "Is the potential high-yield exposure created through P2P lending able to meet my level of acceptable risk?"

Indian POV: Where P2P Fits in a Real Portfolio

If you're an Indian professional trying to manage a lot of debt through EMIs, SIPs and an emergency fund while at the same time building towards using P2P lending in India it will seem more like a 'satellite' investment than just using it as your 'core' or main form of investment. P2P should be viewed as a tactical allocation in the same way you may consider allocating your investments in corporate bond funds or higher yield non-convertible debentures (NCD's). P2P lending should not replace any fixed term deposits (FD's) or liquid funds.

- Currently many financial planners have established a realistic approach for their clients by recommending the following:

- Maintain 6-12 months of expenses in only bank and liquid fund accounts.

- Build your core long-term investment by using equity funds; contribute to your Employee Provident Fund (EPF); invest into your National Pension Scheme (NPS).

- Use 5%-10% of your total financial portfolio to invest in P2P as a higher-yield alternative to equities; start with small amounts, but diversify across multiple platforms/borrower grades.

Business owners can also use P2P as both an alternative source of funding, as well as an investment opportunity, however caution should be exercised regarding conflicts of interest and liquidity when combining these functions.

What to Watch Before You Click “Invest”

Prior to pursuing higher returns than traditional savings, review the following: default and recovery rates by vintage year rather than just averages based on shiny IRRs.

How much you can diversify (number of loans and amount of money loaned to each borrower). Governance of the platform, audited history, and if it's registered with RBI.

In a world where people are increasingly turning away from banks, P2P lending is an incredibly effective way to invest—if you're treating it like credit investment rather than an enhanced savings account.

Latest Posts